Energy Web (EWT)

By Chris Kilbourn | Crescent City Capital Market Analyst Intern

Energy Web

As the repercussions of COVID-era monetary policy conspire with the West’s economic decoupling from Russia, energy is likely to see continued price volatility and likely shortages around the world. Shortages can be mitigated by grid operators through supplementation with Distributed Energy Resources (DERs), but distributed generation requires digital infrastructure to mediate energy flows between large numbers of independent actors. A variety of blockchain solutions have emerged which attempt to provide this infrastructure, some more ambitious than others. While competitors offer more prescriptive protocols with designs on disrupting existing industry, Energy Web provides an ecosystem in which energy-centric dApps can be developed by utility companies themselves. For the scalability of its product and its integration with existing energy infrastructure, Energy Web is significantly more likely than its competitors to capitalize on the ongoing introduction of renewable energy sources to the grid, the transition to a distributed energy marketplace, and the newfound upheaval in the supply chains of the global energy market.

Qualitative Analysis

The utility sector has long been a centralized industry with little room for radical disruption, as grids have historically involved the one-way transmission of power from centralized generators to retail. The past decade has seen the introduction of a new generation of DERs in the form of electric vehicles and small-scale generators, which allow consumers at the distribution level to support the grid by selling excess energy back into the system. The ongoing incorporation of these resources by utility companies promises to not only introduce more renewable energy to existing grids, but also to ameliorate inefficiencies using distributed and data-driven energy flows.

A number of existing blockchain solutions provide models for building out these networks, but because the utility sector is a crowded field with both entrenched interests and implications for national security, any changes require piecemeal alterations to existing systems and partnerships with existing industry, as opposed to radically new models. This will almost certainly take the form of utility companies evolving their monopoly on the transmission of power to include the ownership of networks through which end users buy and sell energy resources amongst each other.

The Energy Web Chain

Energy Web’s protocol is a layer one blockchain that facilitates the construction of these networks in several ways. On top of its consensus layer is a “utility layer” that provides basic infrastructure like bridges and oracles, which are necessary for the purchase and transfer of EWT and the transmission of data relevant to measuring energy flows, respectively. The utility layer supports the development of independent enterprise-grade applications, but a simpler solution also exists.

On top of this layer is a “toolkit layer” with templates that grid operators can use to quickly develop their own apps using Energy Web’s software development kit. These dApps generally take the form of operating systems for upgraded, distributed energy grids, which are based on Energy Web’s virtual machine, EW-DOS. The most important capabilities of these applications are the integration of retail DER devices onto the grid – typically solar panels and EVs – and the construction of on-chain energy markets in which consumers can exchange resources with them. As the Foundation has said in the past, “Our vision is for grid operators to invest in, build, and operate digital systems that securely integrate millions of customers and customer-owned DERs into core operation and planning functions.”

The competitors examined who are working in the same field as Energy Web offered products in the form of dApps for the exchange of energy credits or dApps specifically designed as independent marketplaces for peer-to-peer energy trading in jurisdictions that have completely deregulated the energy market. These appear successful at their own scale, but primarily serve isolated communities and real estate developments that are capable of experimenting with energy alternatives off grid. As a layer-one ecosystem with its own virtual machine upon which enterprise partners can build their own products, EWT seems significantly more scalable and more appealing to the market participants who currently dominate energy distribution.

Partnerships

The conversation around renewable energy is often contentious and presented as a dichotomous choice between green energy and outdated fossil fuels, with the debate polarized by unnecessary political overtones. This is presumably because it has been framed in the past in terms of the wholesale – and unlikely – replacement of the energy sector by tech-centric alternatives, which is naturally an attack on conservative regions whose economies subsist on resource extraction. Energy Web’s single greatest asset is its ability to bridge this divide by formulating a solution that incorporates renewable energy into distributed grids without fundamentally upending the existing order. Three points on that subject:

First, Energy Web was founded by the Rocky Mountain Institute, a non-adversarial think tank with a long history of collaborating with energy and utility companies to develop profitable, market-based innovations.

Second, it has already partnered with energy and utility companies around the world to launch projects using EW-DOS – leaps and bounds beyond any competitors. While similar projects are utilizing less ambitious technology to construct utopian energy communes outside the existing system, Energy Web is already working directly with Shell, GE, Siemens, PG&E, Elia, AES, Duke Energy, Eneco, AEMO, Equinor, and several dozen others in the industry to update existing grids in ways that are beneficial for all parties.

Third, while EW-DOS exists on a permissionless utility layer, consensus occurs on a permissioned “trust layer” on which validator nodes are operated by 25 of these affiliate companies. While such a short list of validators would ordinarily be considered a security risk for a layer one blockchain, this arrangement provides its own kind of security as it is unlikely that vetted, corporate validators will act in bad faith. Perhaps more importantly, it maintains a system in which energy and utility companies are the major stakeholders and cements the Energy Web chain as a product both for and of these massive industries.

Quantitative Analysis

Energy Web has a market cap of $183,857,658 with an FDV of $611,592,090, and EWT has a circulating supply of 30,062,138 out of a max supply of 100,000,000 with no possibility of max supply increase.

Tokenomics

Simply put, EWT has extremely advantageous tokenomics. Energy Web never had an ICO, and there was no point at which the public purchased large amounts of EWT that could be dumped on the market down the road. Its tokens were distributed in eight separate tranches, but these can be simplified to four distinct groups of token holders.

Affiliate investors received 21,198,208 EWT.

Founders received 10,000,000 EWT.

Validators will receive 10,000,000 EWT as block rewards over the next 10 years.

The Energy Web Foundation received 58,801,792 EWT for use in operations and the development of new technologies.

The most significant observation about EWT’s token distribution is that nearly all stakeholders are directly invested in the functioning of EWT’s actual use case. Investors were comprised almost entirely of the affiliate energy and utility companies with whom EWT has partnered. The founders who received 10M EWT are not self-interested individuals, but the two organizations who collaborated to build EWT – Grid Singularity and the Rocky Mountain Institute. Validators are also comprised of major corporations with a vested interest in EWT’s success, and the remaining token distribution went to the Energy Web Foundation, which is headquartered in Switzerland and thus forbidden from having shareholders or seeking profits.

Regarding inflation, staking rewards and community fund tokens represent 48M EWT and will be released over a ten-year period. Community fund tokens have been slated to unlock at 3.79M per year, and block rewards will be released logarithmically at an average of 1M per year. At 4.78 annual inflation of the circulating supply, EWT is highly competitive compared to most other staking-based blockchain protocols.

Price Action

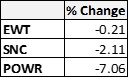

For the immediate future, conditions in the global energy market will be defined by the fracturing of supply chains that followed the Russian invasion of Ukraine, so the relative response of different protocols since that event on February 24th may offer some insight into future performance. POWR and SNC are likely the closest approximations to EWT on the market – though not layer one protocols, both offer peer-to-peer energy marketplaces that should see increased investment as supply issues incentivize diversified forms of energy. Wholly deregulated energy markets exist only overseas, so prices were denominated in BTC.

Bitcoin has seen renewed interest since a bullish narrative emerged around the threat of weaponized financial sanctions, and EWT has moved in tandem with BTC even as its competitors fell increasingly behind. This can be considered strong evidence that EWT’s unique approach to implementing distributed energy and its strong ties to existing industry make it the most likely beneficiary of changing conditions in the current energy market.

This price action has taken place at a time of economic turbulence, before EWT has scratched the surface of its potential for widespread adoption, and while its price against the US Dollar increased by 17.45%. It is the author’s belief that EWT will continue to continue to outperform even in the event of a BTC drawdown as it experiences wider adoption in the face of supply chain difficulties.

Price/Entry

EWT’s current price is $6.099. As with other tokens, Energy Web is naturally correlated with the movements of the broader crypto market, and Bitcoin is currently at a range high of $45,000. If BTC stays rangebound, other tokens will probably retreat as well, and $5.097 sits on a trendline between EWT’s daily lows and its confluence with the 0.618 fib level.

While current catalysts exist to push EWT’s price up, it is important to remember that it also stands to benefit from a long and continuously unfolding process wherein companies in the utility and energy sector will inevitably incorporate developing technologies into their existing business. In the short term, however, EWT exists as a solution to immediate and worsening problems with the world’s energy supplies and will likely attract increasing amounts of clients as these conditions persist. Because of its involvement with an industry that performs one of the bedrock functions of society and its efforts to assist that industry in times of volatility and supply chain difficulties, Energy Web is very likely to outperform the majority of other crypto use cases in times of both inflation and economic downturn.